Manufacturing Sector Working Capital Cycles: What entrepreneurs should be planning for

Impact Partner Content – Absa / by Justin Schmidt, Head of New Sector Development, Absa Retail and Business Bank

Business conditions are improving but supply chain frictions remain

This week the latest Absa Purchasing Managers Index (PMI) data showed further evidence of the continued recovery of the sector with the PMI improving to 57.8 in May. This is the tenth consecutive month that the Absa PMI has been above the 50-point threshold that separates expansion and contraction and shows some promising resilience in the sector. Output and new sales orders continue to see strong reads in this survey.

Unfortunately, we continue to see disruptions to the supply chain and these inefficiencies are an impediment on manufacturer’s road to recovery. Raw material shortages are a major constraint on manufacturers current activity, at a time when manufacturers are seeing greater positivity in terms of future exports and sales. To avoid a lack of inventory compared to what is needed to meet forward looking demand, we have seen some manufacturers restocking extra raw materials to ensure they do not have lost future sales.

Steady rises in producer price indexes as well as elevated levels in the PMI’s purchasing price index will result in margin pressure if these cost pressures cannot be passed through to the end consumer. While the rand strength has offered some relief for imported raw materials, it would be putting pressure on export revenue. The rate of energy increases of 18% in July with put further pressures on margins.

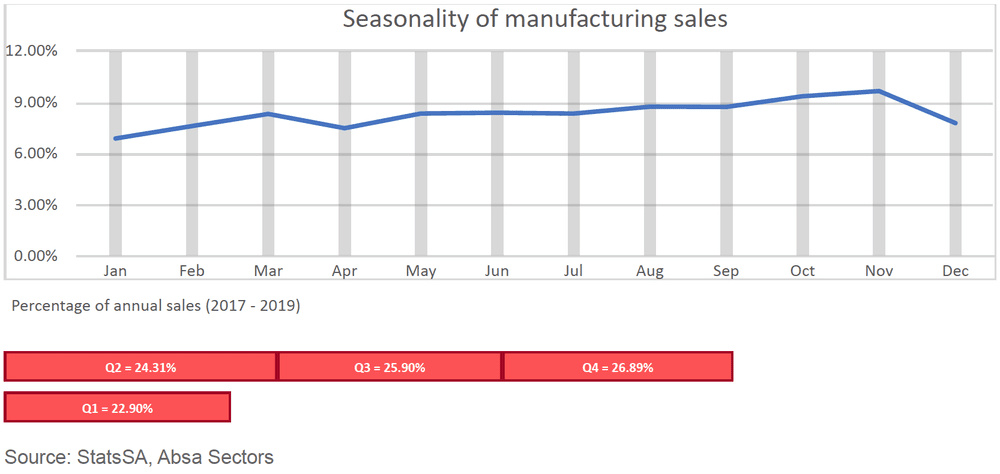

Another important consideration as we move into H2 of 2021 is that we are entering the peak season for manufacturers. Traditionally approximately 53% of sales are achieved in H2 and about 27% in Quarter 4. If we compare sales in Q1 to Q4, sales are, on average, 17% higher in the last quarter of the year:

Analysing the cash conversion cycle (CCC) and understanding how this may be impacting working capital

With the rebound, improved sales outlook, margin constraints, potential stocking up of raw materials and inventory build up to avoid unfulfilled orders as well as higher seasonal sales, the managing of these cash flow constraints is an essential consideration.

Let us consider the cash conversion cycle (CCC) of a business and how capital is tied up at each point in this cycle. The CCC is a measure of how long it takes the company to turn its cash investment in inventory back into cash (from sales of that inventory). The longer the CCC, the greater the amount of capital invested in the sales process. Importantly, when cash is locked up in the sales process, it cannot be used anywhere else in the business. Understanding the cash conversion cycle and it’s three components is key to knowing where short-term capital is tied up:

1. Average Receivables Collection Period

Average Receivables Collection Period (ARCP) measures how long it takes a business to collect the cash from their credit sales to clients. An important consideration is that these sales need to be converted from receivables back into cash – until the money from a sale is paid into the bank account of the business, this cash is tied up as working capital.

2. Average Inventory Processing Period

Average Inventory Processing Period (AIPP) measures how long a business sits on their inventory. With raw material shortages and increased investment into inventory many manufacturers will, in the short-term tie up capital in inventory.

3. Payables Payment Period

Payables Payment Period (PPP) measures how long it takes a business to pay their suppliers.

CCC = ARCP + AIPP – PPP

Understanding the various scenarios of your CCC gives you an understanding of the capital tied up as well as plan how to fund this (cash or short-term funding like overdrafts). To unpack the capital impacts of the current environment on manufacturers, let us assume the below:

Further, to calculate the amount of capital tied up in the CCC, we can use the below calculations:

Working Capital Need

= (Daily Sales x ARCP) + (Daily Cost of Sales x AIPP) – (Daily Cost of Sales x PPP)

Let’s assume the below:

Therefore, if we take the above scenario for a manufacturer as well as the assumed CCC parameters, they would have R5.1m tied up in working capital which would need to be financed through cash or some form of short-term funding.

What are the potential impacts of the current macro environment on the manufacturer?

-

With raw material shortages, supply chain constraints as well as the 18% increase in municipal electricity prices (1 July ’21) let us assume that cost of sales will increase by the latest PPI for April ’21 of 6.7%.

-

Given the raw material shortages we have seen manufacturers order greater quantities of these, therefore let us assume this means higher levels of stock held and increase of AIPP.

-

Many manufacturers cannot pass cost increases on to end users, as they look to maintain or grow market share. Therefore, let us assume sales prices do not increase.

-

Due to seasonality of sales in the sector lets further assume that daily sales in H2 are 7% higher than the daily average for the full year.

-

The changes in assumptions are summarised below:

The combined impact of the above scenario is a working capital need of R6.42m. This equates to approximately a 26% increase in capital tied up in working capital. Although we are seeing good news in terms of the growth momentum and recovery of the manufacturing sector, the raw material shortages and margin pressure are complicating the recovery of manufacturers. In the short to medium term, working capital and the funding thereof will be a key consideration for manufacturers and their stakeholders (including their funding institutions).

Leave a Reply

Want to join the discussion?Feel free to contribute!